Alexandria Ocasio-Cortez Doesn’t Understand How Obamacare’s Exchanges Work

On Twitter Sunday evening, Rep. Alexandria Ocasio-Cortez (D-N.Y.) complained about what she viewed as the daunting prospect of having to choose her health insurance plan for 2020.

It’s not the first time Ocasio-Cortez has taken issue with the health coverage for members of Congress. She griped about the process last year, as a newly elected official just taking her seat.

But, as someone who has gone through the process of buying health insurance as a DC resident for years, I can characterize most of the points she makes in the tweet as inaccurate, or rooted in the special privilege she receives as a member of Congress.

She’s Not Buying ‘Off the Exchange’

To start with, Ocasio-Cortez claimed that “Members of Congress also have to buy their plans off the Exchange.” That statement contains numerous false elements. Most obviously, she cannot buy her insurance off the exchange because the District of Columbia abolished its private insurance market “off the Exchange.”

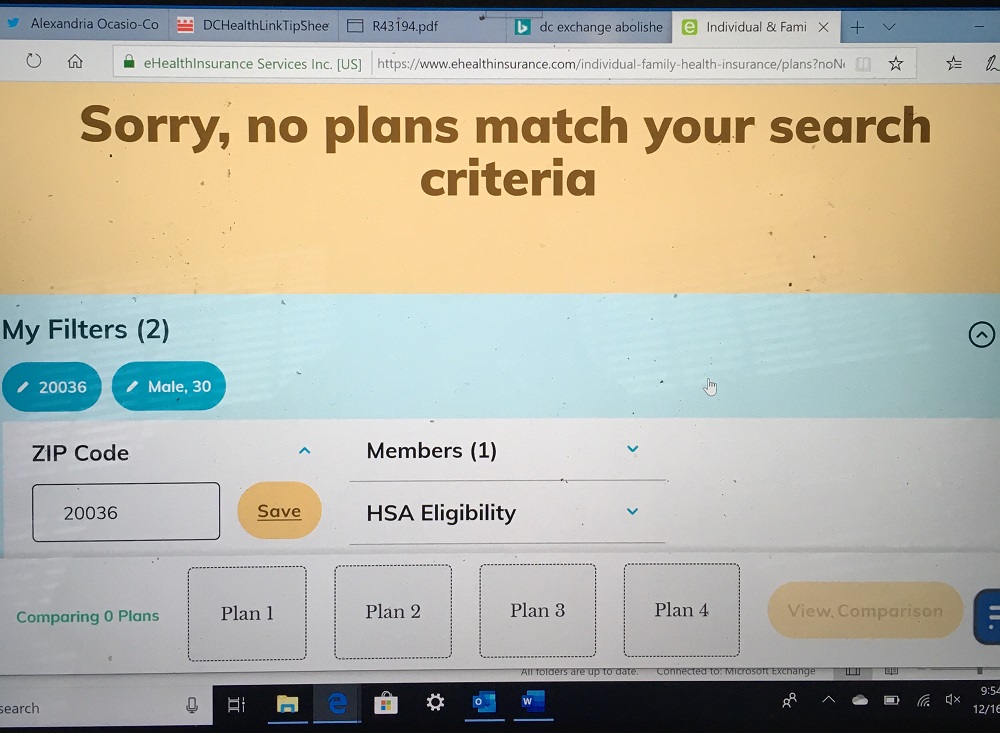

Upon seeing her tweet, I went to eHealthInsurance, a private market away from the government-run exchange, and tried to search for a plan. (Disclosure: I used to represent eHealth more than a decade ago as a paid lobbyist.) When I typed in a DC-based ZIP code, I found the following:

eHealth doesn’t offer insurance plans in the District of Columbia, because it can’t offer them. DC law prohibits anyone but the exchange from selling insurance to individuals.

Rather than purchasing coverage “off the Exchange,” Ocasio-Cortez buys her health insurance through DC’s small business exchange, as opposed to its marketplace for individuals. As a Congressional Research Service paper on health coverage for members of Congress and their staff explains, both groups buy insurance through the DC small business exchange to obtain their (illegal) employer subsidy.

Admittedly, Ocasio-Cortez may have meant “from the Exchange” when she said “off the Exchange.” But her imprecise language implies that she does not understand the important distinction between buying plans from the Exchange directly and not doing so. (Only Exchange-purchased plans qualify for subsidies under the Obamacare statute.)

She Gets Access to More Plans as a Member of Congress

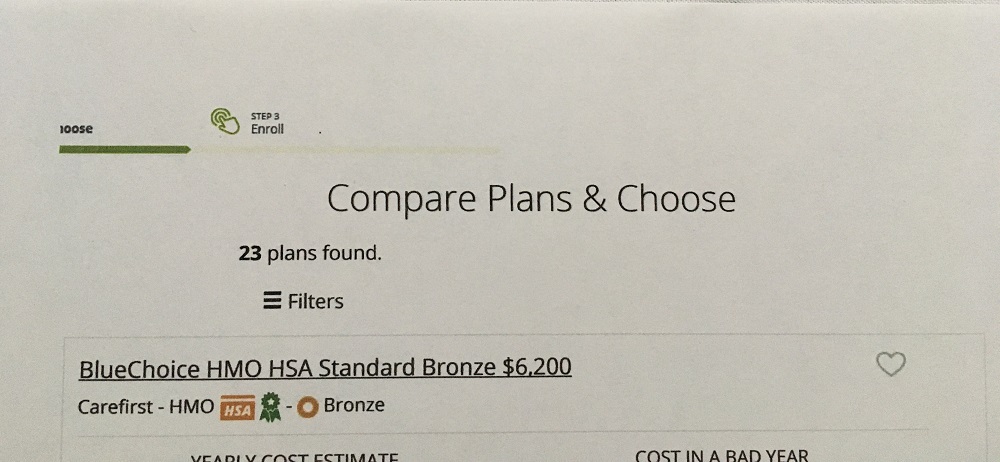

Ocasio-Cortez complained about having to choose from 66 different insurance plans. She wouldn’t have that problem if she weren’t a member of Congress. People who buy insurance on DC’s individual exchange have far fewer options. I know, because I have to buy coverage there. Take a look at the “choices” my personalized webpage presented to me: Only 23 plans—about one-third the number available to Ocasio-Cortez:

Some may think that 23 plans still represent a large number to choose from, but my reality proved far different. To begin with, those plans come from only two carriers: CareFirst Blue Cross Blue Shield and Kaiser Permanente, which only offers HMO options. If you don’t want to get locked into an HMO’s provider network—and I don’t—you have exactly one choice of carrier: CareFirst.

Couple my preference for non-HMO coverage with my desire for insurance that includes a health savings account option, and I ended up with only two plans to choose from: CareFirst’s Bronze HSA plan, and its Gold HSA plan.

I would prefer more choices for health insurance. I would particularly appreciate the opportunity to buy coverage that doesn’t need to comply with the Obamacare insurance regulations that have driven up premiums and priced millions of people out of coverage. But DC’s insurance regulators have prohibited carriers from offering non-complaint plans, because they’re from the government and they’re here to help.

She Gets Special Privileges as a Member of Congress

To say that members of Congress and congressional staff receive kid-glove treatment from the DC small business exchange would put it mildly. This flyer (from 2013) shows that the DC exchange conducted no fewer than 12 separate in-person enrollment events for members and staff during Obamacare’s first open enrollment period.

Congressional staff confirmed to me that the in-person enrollment sessions continued on Capitol Hill this year. Congressional staff also confirmed that House and Senate benefits counselors can walk them through the entire enrollment process.

Even as an individual DC exchange participant, I received no fewer than five separate e-mails, starting on Friday afternoon, reminding me that Sunday represented the last day to sign up for coverage taking effect on January 1. The timing of Ocasio-Cortez’ tweet suggests that she waited until the last minute to examine her coverage options, but she can’t say she wasn’t warned. Maybe if she and her colleagues spent less time focused on impeachment, Ocasio-Cortez could have found more time to select her plan sooner?

Ocasio-Cortez Gets an Illegal Subsidy

I and others have made this point before: members of Congress and their staff represent the only group that can receive a subsidy from their employer on the exchange. That subsidy came through a rule promulgated by the Office of Personnel Management in 2013, but several analyses have called that rule illegal.

Ocasio-Cortez claimed that “Members of Congress have to buy their plans off the Exchange.” Just as the off-exchange claim holds no basis in fact, she and other members of Congress do not have to buy plans via the DC small business exchange. Nothing in law forces them to do so—unless they want to receive the (illegal) subsidy.

In fact, at least one member of Congress has turned down the (illegal) congressional subsidy. Dr. Michael Burgess frequently mentions at hearings, including the House Energy and Commerce Committee hearing on single payer last week, that he buys his own coverage with his own money, not taxpayer funds. As someone who earns less than members of Congress do, and has no access to (illegal) insurance subsidies, I appreciate Burgess’ integrity in this regard.

If Ocasio-Cortez wanted to do something other than complain—and if she didn’t want so many choices—she could ditch the special, and illegal, subsidies she receives as a member of Congress, and buy coverage with the hoi polloi like me. She’s welcome to do so any time she likes, but I’m not holding my breath.

UPDATE: This post was updated after publication to clarify potential interpretations of Ocasio-Cortez’ comments about “off the Exchange” coverage.

This post was originally published at The Federalist.