Is Donald Trump “Sabotaging” Obamacare?

Is Donald Trump “sabotaging” Obamacare? And are he and his administration violating the law to do so?

Democrats intend to make this issue a prime focus of their political messaging ahead of the November elections. And several developments over the month of August — a Government Accountability Office (GAO) report, a New York Times op-ed by two legal scholars, and a lawsuit filed by several cities — all include specific points and charges related to that theme.

1. The GAO Report

The most recent data point comes from the GAO, which at the behest of several congressional Democrats analyzed the administration’s outreach efforts during the most recent open enrollment period last fall. Those efforts culminated in a report GAO released Thursday.

The report made a persuasive case that the administration’s decision to reduce and re-prioritize funding for enrollment navigators utilized flawed data and methods. While the Department of Health and Human Services (HHS) based navigators’ 2018 funding on their effectiveness in enrolling individuals in coverage in prior years, GAO noted that HHS lacked solid data on navigators’ enrollment on which to base 2018 funding, and that enrollment was but one of navigators’ stated goals in prior years. HHS agreed with GAO’s recommendation that it should provide clearer goals and performance metrics for navigators to meet.

GAO also recommended that the administration reinstitute an overall enrollment target, as one way to determine the adequate distribution of resources during open enrollment. However, a cynic might note that Obamacare advocates, including the Democratic lawmakers who requested the report, may want the Trump administration to publicize an enrollment target primarily so they can attack HHS if the department does not achieve its goals.

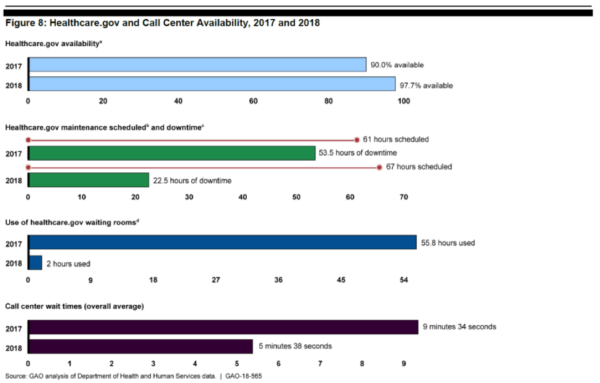

Even though reporters and liberals like Andy Slavitt cried foul last year when HHS announced planned maintenance time for healthcare.gov in advance, actual downtime for the site dropped precipitously in 2018 compared to 2017. Which could lead one to ask who is sabotaging whom.

2. The New York Times Article

In The New York Times piece, law professors Nicholas Bagley and Abbe Gluck provide an overview of the lawsuit filed against the Trump Administration (about which more below). As someone who has cited Bagley’s work in the past, I find the article unpersuasive, even disappointing.

Take for instance some of the article’s specific allegations:

Here’s one: “To make it harder for people to enroll in Obamacare plans, for example, the administration shortened the open enrollment period on the health care exchanges from three months to six weeks.”

This charge would have evaporated entirely had Bagley specified which Administration first proposed shortening the open enrollment period to six weeks. The Obama Administration did just that.

This rule also establishes dates for the individual market annual open enrollment period for future benefit years. For 2017 and 2018, we will maintain the same open enrollment period we adopted for 2016—that is, November 1 of the year preceding the benefit year through January 31 of the benefit year, and for 2019 and later benefit years, we are establishing an open enrollment period of November 1 through December 15 of the year preceding the benefit year.

The Trump administration merely took the shorter open enrollment period that the Obama team proposed for 2019 and accelerated it by one year. If shortening the enrollment period would make it so much “harder for people to enroll in Obamacare plans,” as Bagley and Gluck claim, then why did the Obama Administration propose this change?

Another allegation: “To sow chaos in the insurance markets, Mr. Trump toyed for nine months with the idea of eliminating a crucial funding stream for Obamacare known as cost-sharing payments. After he cut off those funds, he boasted that Obamacare was ‘being dismantled.’”

This charge seems particularly specious — because Bagley himself has admitted that Obamacare lacks a constitutional appropriation for the cost-sharing reduction payments to insurers. Bagley previously mentioned that he took no small amount of grief from the left for conceding that President Obama had exceeded his constitutional authority. For him to turn around and now claim that Trump violated his constitutional authority by ending unconstitutional payments represents a disingenuous argument.

Here and elsewhere, Bagley might argue that Trump’s rhetoric — talk of Obamacare “being dismantled,” for instance — suggests corrupt intent. I will gladly stipulate that presidential claims Obamacare is “dead” are both inaccurate and unhelpful. But regardless of what the President says, if the President does what Bagley himself thinks necessary to comport with the Constitution, how on earth can Bagley criticize him for violating his oath of office?

A third allegation:

This month, the Trump administration dealt what may be its biggest blow yet to the insurance markets. In a new rule, it announced that insurers will have more latitude to sell ‘short-term’ health plans that are exempt from the Affordable Care Act’s rules. These plans … had previously been limited to three months.

Under Mr. Trump’s new rule, however, such plans can last for 364 days and can be renewed for up to three years. … In effect, these rules are creating a cheap form of ‘junk’ coverage that does not have to meet the higher standards of Obamacare. This sort of splintering of the insurance markets is not allowed under the Affordable Care Act as Congress drafted it.

This claim also fails on multiple levels. First, if Congress wanted to prohibit “short-term” health plans as part of Obamacare, it could have done so. Congress chose first to allow these plans to continue to exist, and second to exempt these plans from all of Obamacare’s regulatory regime. If Bagley and Gluck have an objection to the splintering of insurance markets, then they should take it up with Congress.

Second, the so-called “new rule” Bagley and Gluck refer to only reverts back to a definition of short-term coverage that existed under the Obama Administration. This definition existed for nearly two decades, from when Congress passed the Health Insurance Portability and Accountability Act (HIPAA) through 2016. The Obama administration published a rule intended to eliminate much of the market for this type of coverage — but it did so only in the fall of that year, more than two years after Obamacare’s major coverage provisions took effect.

As with the shortening of the open enrollment period discussed above, if Bagley and Gluck want to scream “Sabotage!” regarding the Trump administration’s actions, they also must point the finger at Barack Obama for similar actions. That they did not suggests the partisan, and ultimately flawed, nature of their analysis.

3. The Lawsuit

The 128-page complaint filed by the city plaintiffs earlier this month makes some of the same points as the New York Times op-ed. It also continues the same pattern of blaming the Trump administration for actions previously taken by the Obama administration.

The lawsuit criticizes numerous elements of the administration’s April rule setting out the payment parameters for the 2019 Exchange year. For instance, it criticizes the removal of language requiring Exchanges to provide a direct notification to individuals before discontinuing their eligibility for subsidies, if individuals fail to reconcile the subsidies they received in prior years with the amount they qualified for based on their income. (Estimated subsidies, which are based on projected income for a year, can vary significantly from the actual subsidy levels one qualifies for, based on changes in income due to a promotion, change in life status, etc.)

As part of this charge, the lawsuit includes an important nugget: The relevant regulation “was amended in 2016 to specify that an Exchange may not deny [subsidies] under this provision ‘unless direct notification is first sent to the tax filer.’” As with the New York Times op-ed outlined above, those claiming “sabotage” are doing so because the Trump administration decided to revert to a prior regulatory definition used by the Obama administration for the first several years of Obamacare implementation.

The lawsuit similarly complains that the Trump administration is “making it harder to compare insurance plans” by eliminating support for “standardized options” from the Exchange. Here again, the complaint notes that “prior rules supported ‘standardized options,’” while mentioning only in a footnote that the rules implementing the “standardized options” took effect for the 2017 plan year. In other words, the Obama administration did not establish “standardized options” for the 2014, 2015, or 2016 plan years. Were they “sabotaging” Obamacare by failing to do so?

The suit continues with these types of claims, which collectively amount to legalistic whining that the Trump administration has not implemented Obamacare in a manner the (liberal) plaintiffs would support. It even includes this noteworthy assertion:

Maryland has been cleared by state legislators to petition CMS to ‘establish a reinsurance program that would create a pot of money for insurers to cover the most expensive claims,’ but a health economist ‘said he would be shocked if the Trump administration approved such a request, given its efforts to weaken Obamacare’: ‘It just seems very unlikely to me that Trump would approve this. … Maryland is easily saying we want to help prop up Obamacare, which the Trump administration doesn’t want to have anything to do with.’

Fact: The Trump administration just approved Maryland’s insurance waiver this week. So much for that “sabotage.”

A review of its “prayer for relief” — the plaintiffs’ request for actions the court should take — shows the ridiculously sweeping nature of the lawsuit’s claims. Among other things, the plaintiffs want the court to order the defendants to “comply with their constitutional obligation to take care to faithfully execute the ACA,” including by doing the following:

- “Expand, rather than suppress, the number of individuals and families obtaining health insurance through ACA exchanges;

- “Reduce, rather than increase, premiums for health insurance in the ACA exchanges;

- “Promote, rather than diminish, the availability of comprehensive, reasonably-priced health insurance for individuals and families with preexisting conditions;

- “Encourage, rather than discourage, individuals and families to obtain health insurance that provides the coverage that Congress, in the ACA, determined is necessary to protect American families against the physical and economic devastation that results from lesser insurance, with limits on coverage that leaves them unable to cover the costs of an accident or unexpected illness…

- “Order Defendants to fully fund advertising under the ACA;

- “Enjoin Defendants from producing and disseminating advertisements that aim to undermine the ACA;

- “Order Defendants to fully fund Navigators under the ACA;

- “Enjoin Defendants from incentivizing Navigators to advertise non-ACA compliant plans;

- “Order Defendants to lengthen the open enrollment period;

- “Order Defendants to resume participation in enrollment events and other outreach activities under the ACA…

- “Order Defendants to process states’ waiver applications under the ACA so as to faithfully implement the Act.”

In other words, the lawsuit asks a court to micro-manage every possible element of implementation of a 2,700-page law — tell HHS what it must say, what it must do, how much it must spend, and on and on. It would create de facto entitlements, by stating that HHS could never reduce funding for advertising and outreach, or lower spending on navigators, or reject states’ waiver applications — potentially even if those applications violate the law itself. And it asks for impossible actions — because HHS cannot unilaterally “expand, rather than suppress” the number of people with coverage, just as it cannot unilaterally “reduce, rather than increase, premiums.”

Despite its questionable claims, and the highly questionable remedies it seeks, the lawsuit may yet accomplish some of its goals. The complaint spends much of its time alleging violations of the Administrative Procedure Act, claiming that HHS did not “meaningfully” or “adequately” consider comments from individuals who objected to the regulatory changes in question. While I have not examined the relevant regulatory dockets in any level of detail, the (pardon the pun) trumped-up nature of elements of the complaint makes me skeptical of such assertions. That said, the administration has suffered several setbacks in court over complaints regarding the regulatory process, so the lawsuit may force HHS to ensure it has its proverbial “i”s dotted and “t”s crossed before proceeding with further changes.

Words Versus Actions

On many levels, the “sabotage” allegations try to use the president’s own words (and tweets) against him. Other lawsuits have done likewise, with varying degrees of success. As I noted above, the president’s rhetoric often does not reflect the actual reality that Obamacare remains much more entrenched than conservatives like myself would like.

But for all their complaints about the administration’s “sabotage,” liberals have no one to blame but themselves for the current situation. Obamacare gave a tremendous amount of authority to the federal bureaucracy to implement its myriad edicts. They should not be surprised when someone who disagrees with them uses that vast power to accomplish what they view as malign ends. Perhaps next time they should think again before proceeding down a road that gives government such significant authority. They won’t, but they should.

This post was originally published at The Federalist.